Stock still

How to reform social housing

Britain’s social housing system is badly dysfunctional. Non-portability of tenancies prevents social tenants living where they wish, making them 70% less likely to move home per year than private renters. The system accounts for 23% of London’s housing stock, and still fails the people it is for: waitlists in several boroughs exceed a century, and over 169,000 children are stuck in temporary accommodation. I here build a heterogeneous-agent Rosen-Roback model, and find that social housing causes an output loss of £10.6bn/annum while raising market rents by 8.7% in London and 7.2% nationally; the marginal home let socially rather than at market rates in London forgoes £1.2mn of output present value (PV).

There is a better way. We can simultaneously boost output, benefit both current and future tenants and produce a saving for the exchequer. I model replacing social housing with a voucher calibrated to 30th percentile private sector rents, indexed by household size, while grandfathering in all current social housing tenants. This would realise 96% of the growth gains (£10.2bn) and 85% of the transfer efficiency gains (£7.9bn), while benefitting those who would otherwise be on social housing by £7.6bn/annum EV and saving the exchequer £7.1bn/annum in the long run. Because the voucher would be guaranteed rather than rationed, low-income households would no longer need to wait for a scarce social tenancy before receiving support: the Treasury would gain £120bn PV pre-growth if the stock was given to current occupants, or £508bn PV if it was released to the market as tenancies naturally end.

Model

Suppose we want to estimate the efficiency impact of social housing - what do we need for this? Firstly, we need to know why to care about allocation at all. Cities differ in output by more than they differ in observed skills, hence individuals can frequently earn more by moving to a larger city. The main theory that explains this is agglomeration: individuals are more productive when they have access to a large labour market to interact with.

Standard models, such as Hsieh and Moretti (2019), or Duranton and Puga (2019), both rely on modelling how homogenous labour sorts in response to heterogeneous productivity and amenities across cities. This is unattractive for our purposes for two reasons. Firstly, as social housing is an allocation distortion, labour cannot be modelled as homogenous. Secondly, very large differences in non-agglomeration TFP are hard to believe: local governance differs little, and the public capital stock is too small to drive large gaps here.

Instead, we’ll use heterogeneous worker skill. Why does this matter? Housing demand empirically has an income elasticity of demand below 1: when an individual gets richer by 1%, their housing consumption grows by less than 1%. As wages scale 1-1 with productivity, location in high productivity cities will be relatively less costly for high skill than low skill consumers, as a lower share of their budget is spent on rent. High skill workers thus endogenously sort into large cities, so large cities will be more productive due to both sorting and agglomeration. Social housing is economically costly by preventing mobility to where individuals would freely choose, inhibiting agglomeration and by distorting consumption choices.1

Specifically, we’ll use a Cobb Douglas production function with agglomeration’s productivity effect linear in log aggregate human capital. Workers have Stone-Geary utility over goods, with Frechet preferences over location; cities have identical TFP pre-agglomeration and some amenity level. This means that each location has an effective supply curve of workers: some workers are more attached to their current location, others more indifferent. Amenities are then back-fitted to current destinations to exactly replicate observed populations and wages.

In general, this model has multiple equilibria, as there are increasing returns within each city - if 13th century planning regulation had been more forgiving, Northampton might be a high wage hub rather than Oxford.2 We therefore compute the equilibrium reached by relaxing the social housing constraint in small increments from the status quo: continuously connected to the current allocation, and the one a gradual grandfathered release would be most likely to reach in practice.

Data and parameters

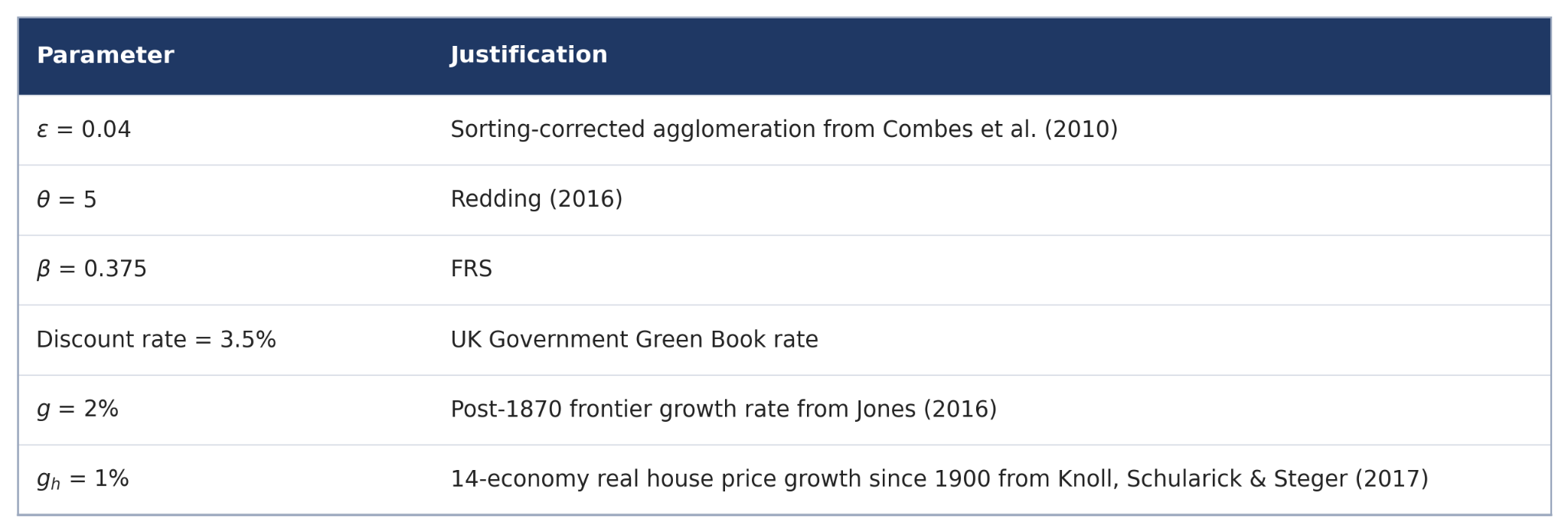

Our unit of analysis is the Travel to Work Area (TTWA): England is split into 151 such units, as the approximation of the local labour market. We use ONS ASHE data on earnings, and Family Resources Survey (FRS) data on rents by TTWA. For data on social households income and other characteristics, we use the English Housing Survey; preferences are also estimated from here. Social housing is devolved so we restrict our focus to England throughout.

Results

We want to ask several questions. Firstly, in this model with heterogenous human capital, how do the output effects of general planning liberalisation compare to the results in a homogenous version? A previous homogenous model, Cooped Up, provided an output effect of 6% under its central imperfect mobility case: this model finds 5.9% for general liberalisation. This is because our model moves results in two directions. Firstly, London’s current wages partly reflect sorting (53% of the wage premium in our calibration), meaning that the productivity effect is correspondingly smaller. Secondly, unlike in Cooped Up cities have increasing not decreasing returns to scale in output, so every new entrant also makes the current population more productive.3 The first effect is slightly larger in practice, especially for large shocks, so the estimated output gain here falls somewhat: under the stretch case of Cooped Up where output grows by 10%, output grows by 7.9% in this model.

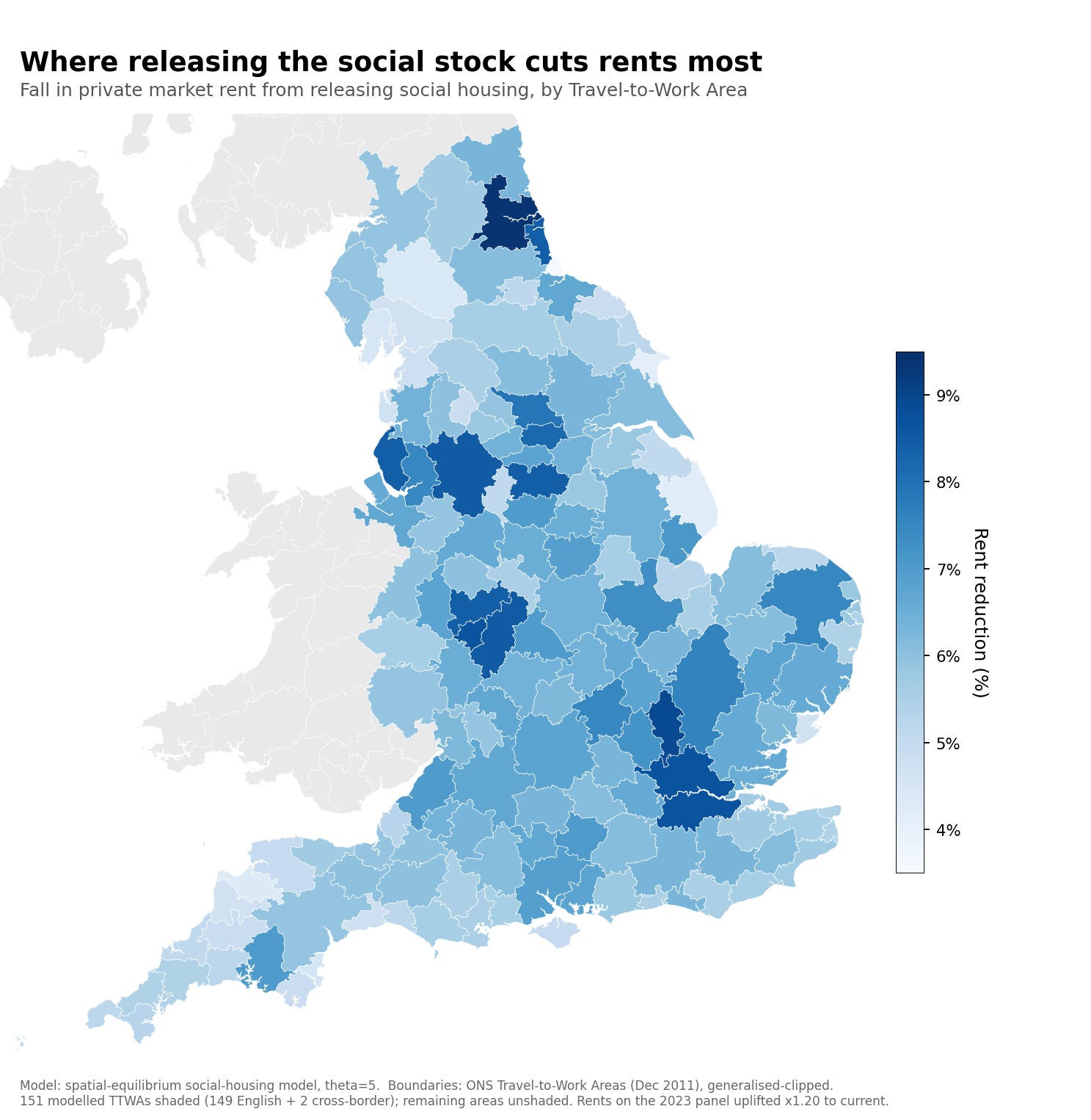

Secondly, what would happen if, in the long run, all council housing entered the market? Output would grow by £10.6bn (0.34%) if the entire national social housing stock enters the market, with market rents falling by 8.7% in London and 7.2% nationally. The total welfare gain is greater than this. This is because social housing is, absent paternalist considerations (and note the rest of the benefit system is delivered as cash), less efficient than cash transfers at delivering welfare to tenants - the implicit share of consumption including imputed rent spent on housing is enormous. Hence, under the utility functions here social housing makes tenants take a higher share of their consumption as housing than they would freely pick given the same resource budget. In this calibration, on the transfer side, social housing is 64% as efficient as cash transfers at delivering utility. The net housing transfer is £25.4bn, hence the value loss on the transfer side is £9.2bn.4 The total welfare loss is the output loss plus the transfer inefficiency, hence total deadweight loss is £19.8bn from the system.5

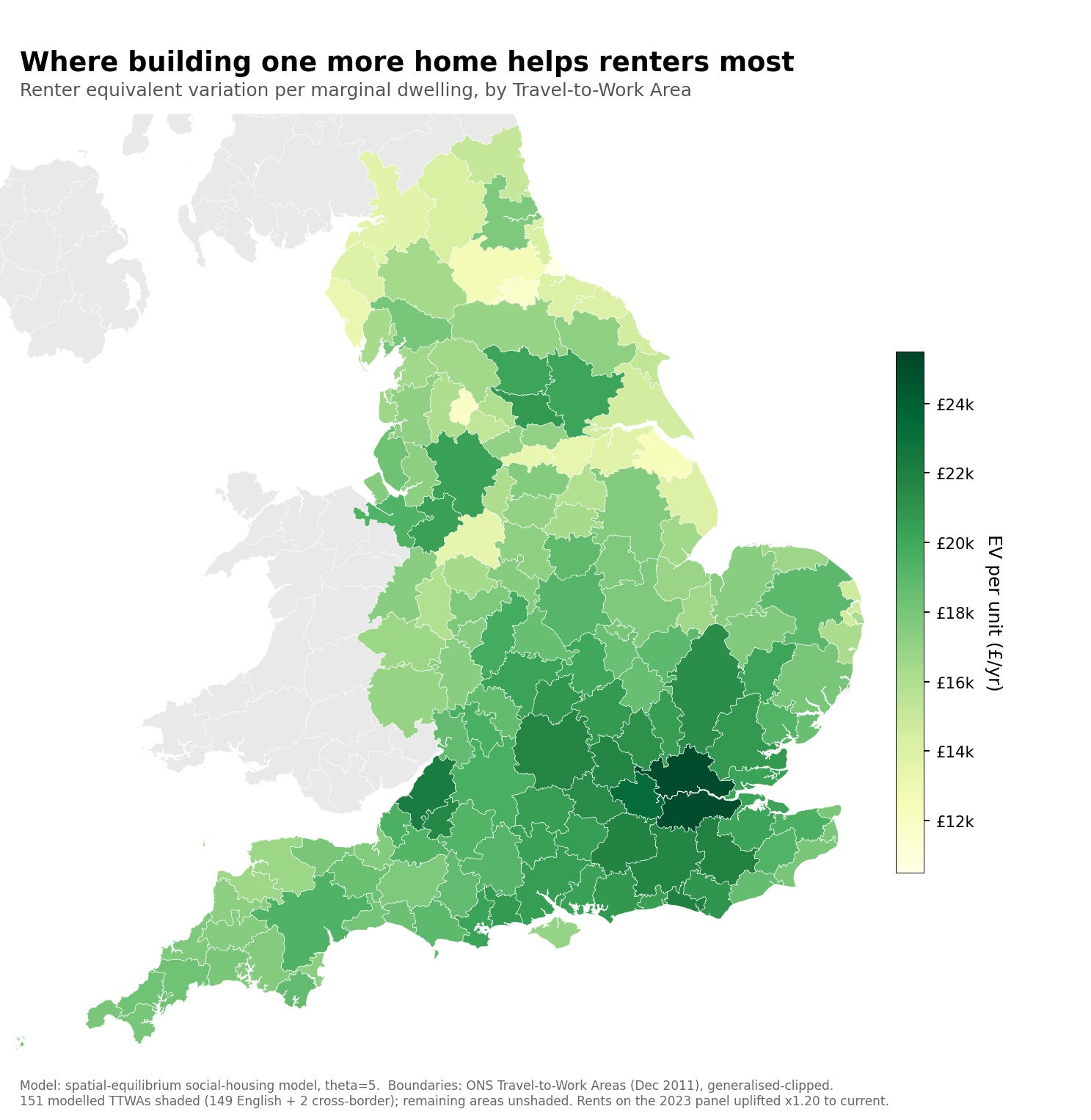

Thirdly, what is the output gain on the margin from one new home in London? A new house built and let at market rate has a modelled output effect is £22,962/annum; if let under the social housing system, the modelled output effect is £5,100/annum. In other words, a social housing unit let on the margin represents the counterfactual loss of £1.2mn PV versus being let at market rate.6 The rent subsidy embedded must itself be tax funded, raising DWL further due to the increased need for other distortionary taxes.7

Policy

How can we reduce the deadweight loss (DWL) of social housing, without hurting current tenants? The primary distortion of social housing is the location distortion: individuals awarded social housing cannot move to their most preferred location with the imputed rent of the property. Hence, the solution is to replace social housing with an earmarked voucher tethered to 30th percentile national private sector rents (such that a couple can afford a 1-bedroom, and a couple with 2 children a 3-bedroom), that is part of universal credit (and tapered as such) and consists of a lump sum per adult and child.

This has several advantages. By using vouchers, tenants will be entirely mobile: and as the voucher is dynamically pegged to national rents, there will be sufficient properties at appropriate sizes; and as the voucher is earmarked it can be sent directly to housing providers with no risk of arrears, hence preventing one of the primary routes causing vouchers to not be accepted in similar programmes abroad. As it is part of universal credit and tapered, it is naturally targeted, while as it is a voucher there is no need for a waitlist, as social housing currently has. As it is a fixed lump sum per adult and child - set per capita so that a family of 4 has sufficient space - it will not discourage family formation. Specifically, at present such a voucher would run to £3300/adult and £1800/child (matching 30th percentile 1 bed at £6600/annum, and 30th percentile 3 bed at £10,200/annum).8

This would replace the redistributive function of the social housing stock: some government-run housing would likely need to still persist, both as temporary accommodation to prevent homelessness of children and several much smaller components for vulnerable groups, but these can be separately run by the relevant departments. Earmarking the voucher realises a £1.35bn transfer efficiency loss, but retains the guarantee of housing hence will be headlined here. Counterfactually-social housing tenants would gain £7.6bn/annum in equivalent variation (EV).

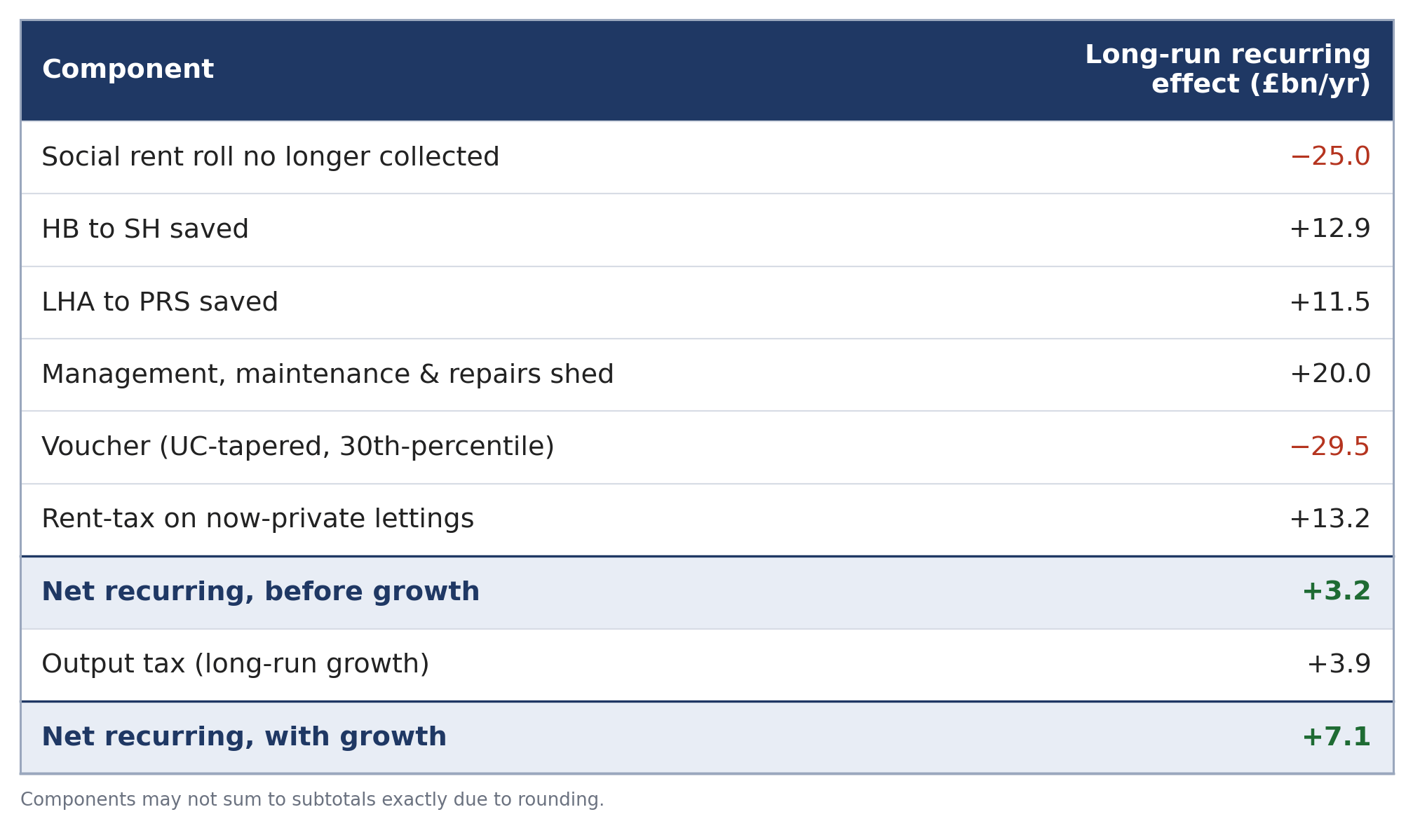

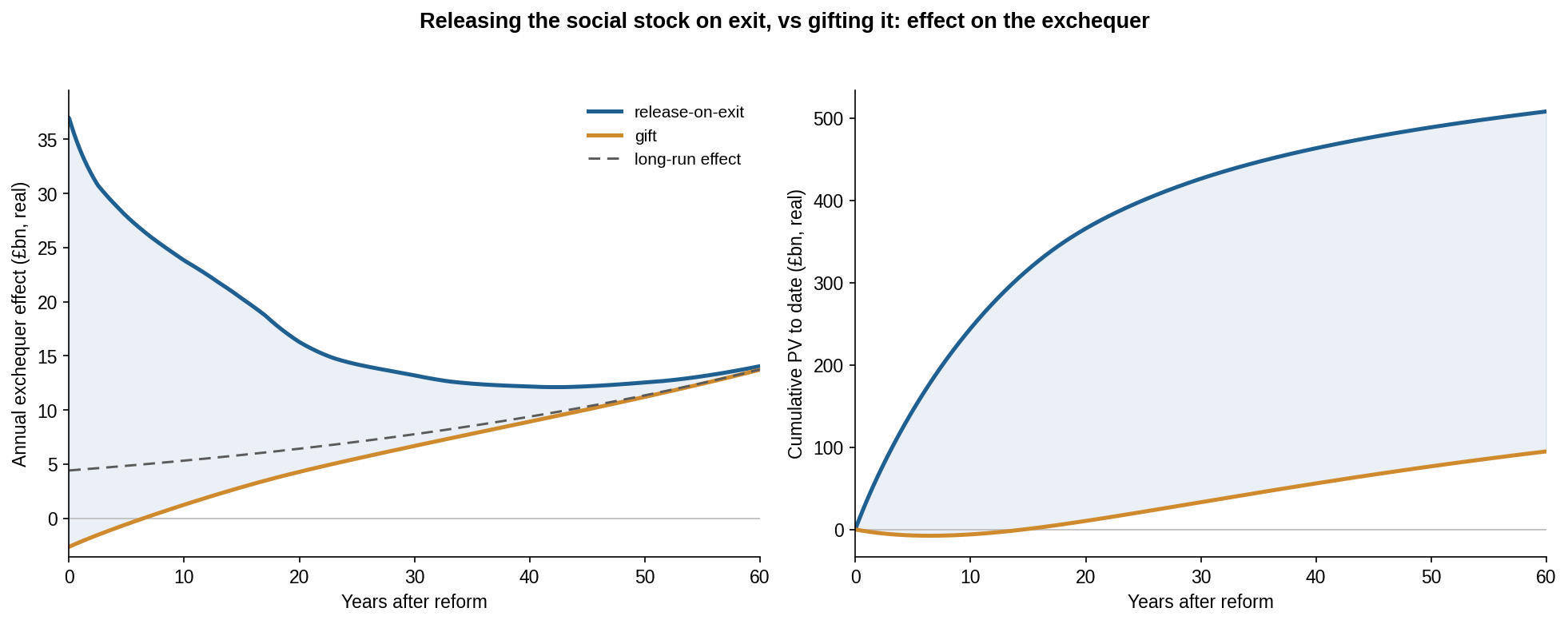

How much would this cost? Surprisingly, the fiscal impact is long run +£3.2bn without accounting for any of the growth impacts, and even more positive at +£7.1bn including them. This is because social rents have often fallen close to the level necessary to cover operations and maintenance, hence releasing current social homes would not be a net fiscal cost as the rent post housing benefit paid is comparable to the maintenance bill and this will now be borne privately. Additionally, much of the rent will be recycled back to the exchequer via taxation of landlords income.9

Given this can replace the system for new entrants, there are several policies we can consider in relation to the current stock while benefitting current tenants. We could expand right to buy (RTB) discounts; directly award all current tenants their homes; or simply cease re-issuing new tenancies on tenants leaving.

RTB discount expansion, while the historical route, is limited by most social housing tenants currently being credit constrained. At present, the annual flow of social housing off government books due to right to buy is only 0.2% of the stock per year: in the model, at the existing tenant distribution discounts would need to be enormous - in excess of 75% - to introduce any substantial exit, and would do so least in London.10

Directly awarding tenants their homes would enable the completion of the transition in one step and create a large constituency with a stake in the new system. While there could be some mobility induced from tenants given their homes in this way, this may be low due to endowment effects, transaction costs (such as stamp duty) and the relatively high average age of tenants. However, it would represent the loss of a £552bn asset; the government would only realise £95bn PV in additional tax, primarily from the output gains.

Lastly, we could cease to issue new tenancies when the property would revert to the council, and sell the property instead. This would at the frequency of tenancies ending in the model result in the policy having a total fiscal PV of £508bn.11 Growth could also be faster if the government also offered to assume the house early in exchange for paying an annuity to tenants equal to the rental value of the property. This would be fiscally neutral, but would allow the realisation of the mobility gains more quickly.

Conclusion

Social housing is not costly because it is a transfer system. Social housing is costly because it spends heavily to prevent many of Britain’s tenants moving where they would wish. An alternative voucher system that offers a guaranteed not rationed housing entitlement could improve welfare by £18bn/annum and benefit the exchequer by £7.1bn/annum. Because every tenant would be grandfathered, current tenants would be secure: the reform would only reach new entrants, who would be better off by £7.6bn/year EV total. The advantage of pro-growth reforms is that they generate sufficient surplus to ensure all groups can benefit.

In principle, the mechanism is also compatible with forced underconsumption: as housing must generally be bought in discrete lumps, if social housing subsidised living in a smaller unit than a family would purchase on the market then they may choose to retain that smaller unit - due to the subsidy - even if their preference would be for a larger one. Replacing with a voucher (as below) corrects for this and allows them to move to a house of their choice.

Northampton had a university in the 13th century that Henry III dissolved by royal decree in 1265 under pressure from Oxford and Cambridge.

Productivity falls in the city sending emigrants, but if mobility is on net to larger cities - as it is in this setting - then this effect is smaller. Specifically, suppose two cities with populations a and b, a + b = 1. Output Y = a^1.04 + b^1.04, hence dY/da / dY/db > 1 if a > b. Note welfare changes in each city will be smaller than this as housing per capita will increase in the sending city and reduce in the receiving city.

Gross value (£37.5bn) less social rent (£25.0bn) plus housing benefit (£12.9bn).

Specifically, they add because output measures the change in production independent of allocation, and transfer inefficiency represents a separate problem of goods received being valued at less than cost.

Insofar as the housing supply curve is not perfectly inelastic this imposes an additional DWL: we do not model this here as the elasticity is likely low in practice.

The subsidy dynamically raises rents, but not by much: the effect is just over 1%, raising the 3-bedroom price from £10,133 to £10,269.

Landlords are modelled as paying an effective rate of 30% on income then 15% on subsequent consumption.

If social rent paid counted towards RTB - as is sometimes suggested - this would be effectively equivalent to the next policy.

Gains are somewhat lower than the headline value of the asset stock because many of the houses are only released decades hence; additionally, net social rent is lower than maintenance obligations hence the gift would actually be more fiscally beneficial in the short run.

Really enjoyed this! I'd enjoy a follow up with some speculation on political feasibility.

Incredibly interesting!